Understanding your home's equity

Homeownership has many benefits, including the opportunity to build wealth over time through equity.

Homeownership has cemented its role as part of the American Dream, providing families with a place that is their own and an avenue for building wealth over time. This "wealth" is built, in large part, through the creation of equity.

But what exactly is equity?

In the simplest terms, your home’s equity is the difference between how much your home is worth and how much you owe on your mortgage.

Look at this example:

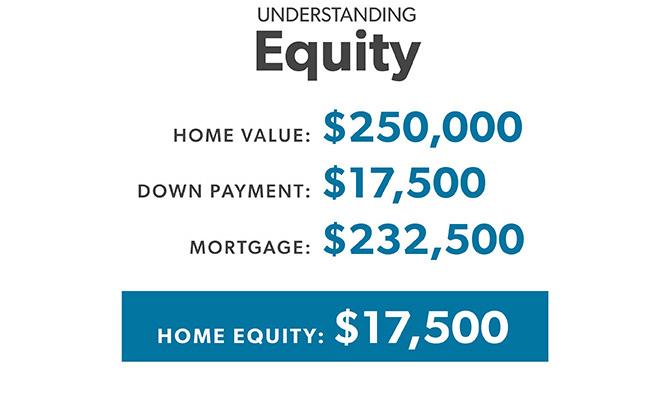

Let's say you bought a $250,000 house with a down payment of 7% (approximately $17,500), resulting in a loan amount of $232,500. By securing a 30-year fixed-rate mortgage at 4.5%, your monthly mortgage payment is $1,178 without taxes and insurance.

To calculate your home equity, subtract the amount of the outstanding mortgage loan from the price paid for the property. Or you can use our home equity calculator.

At the time you buy, your home equity would be $17,500 or the amount of your down payment. For perspective, once you have paid off your mortgage you’ll have 100% equity in the home.

So, how do you build equity?

You build equity in two ways: by paying down your mortgage over time and through your home's appreciation.

Paying your mortgage

Each month, you will make mortgage payments that will decrease the amount you owe on your loan. To see how this works, learn about amortization.

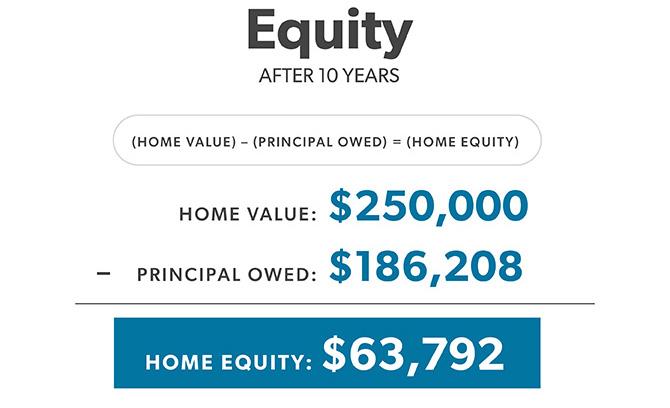

Continuing with our previous example, let's look how your equity would increase after ten years of mortgage payments. After ten years, the unpaid principal balance (the amount you owe) on your mortgage is down to $186,208.

Using the formula from above, your total equity is now $63,792. Note, this is your total equity only if the value of the property remains the same as it was ten years ago – which is where appreciation factors in.

Appreciation

Over time it is unlikely the value of your property will remain the same as when you originally purchased it. While property values can go up or down, the national average for home appreciation is 3% per year. If you live in a neighborhood where property values are going up overall and you’ve maintained your property well, the amount of your equity will increase as well.

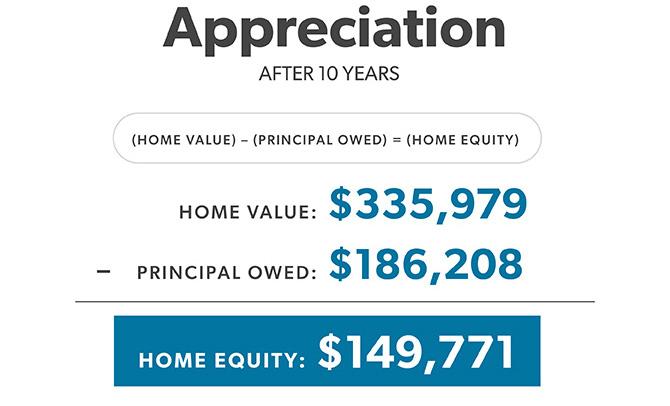

In our example, if your home appreciated by 3% annually, your home's value would increase from $250,000 to $335,979 after ten years. That's a 34% increase in value.

Using the formula from above (home value) – (principal owed) = (home equity) you would have $149,771 in equity.

Building equity through your monthly principal payments and appreciation is a critical part of homeownership that can help you create financial stability. It's important to note that some markets appreciate faster than others. It's also possible for home values to depreciate due to economic conditions, your home not being kept up or a drop in neighborhood home values.

Related Topic

Understanding amortization

Learn about the amortization table and schedule you’ll receive at closing.

Tools and Resources

Brochure: Caring for Your Home

Understand the importance of maintaining your property and how to plan for the unexpected.

Calculator: Home equity

Find out how much equity you have in your home.

Video: Maintaining your Home

Learn how to save for your home’s upkeep.